Abid

Abid- 22 Mar, 2026

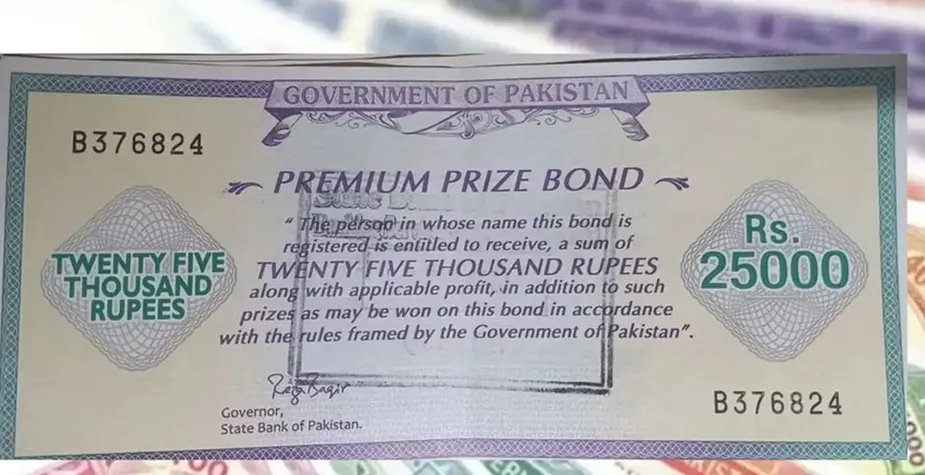

Top 5 National Savings Products in Pakistan

Defence, Behbood, Regular Income Certificates, Prize Bonds, and Premium Prize Bonds compared for savers who want government-backed options in Pakistan.

Read articleAbidDefence, Behbood, Regular Income Certificates, Prize Bonds, and Premium Prize Bonds compared for savers who want government-backed options in Pakistan.

Read article Abid

AbidPak-Qatar, EFU Takaful, Jubilee General Takaful, Dawood Family Takaful, and Salaam Takaful reviewed for Pakistani retail users.

Read article Abid

AbidMeezan, UBL, NIT, Alfalah, and MCB Arif Habib compared for Pakistanis choosing a retail mutual fund platform.

Read article Abid

AbidJS Global, AKD Securities, KTrade, Arif Habib Limited, and Finqalab reviewed through the lens of everyday retail investing in Pakistan.

Read article Abid

AbidRaast, 1LINK, PayPak, MNET Switch, and Visa / Mastercard explained through the payment rails Pakistanis use every day.

Read article