Abid

Abid- 29 Apr, 2026

Getting Started with Investing in Pakistan: A Beginner Guide

Start investing in Pakistan with a clear path from savings accounts and money market funds to deposits, sukuks, metals, currency, PSX, and index funds.

Read articleCategory Archive

Start with regulated channels, account setup basics, risk controls, and practical first steps for Pakistan-based investors.

14 articles in this category.

AbidStart investing in Pakistan with a clear path from savings accounts and money market funds to deposits, sukuks, metals, currency, PSX, and index funds.

Read article Abid

AbidState Life, EFU Life, Jubilee Life, Adamjee, and TPL compared for Pakistanis choosing conventional insurance cover.

Read article Abid

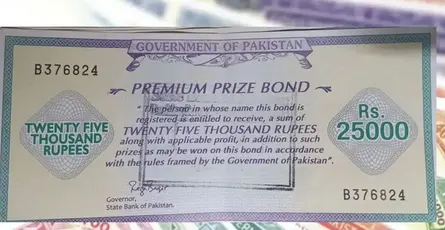

AbidDefence, Behbood, Regular Income Certificates, Prize Bonds, and Premium Prize Bonds compared for savers who want government-backed options in Pakistan.

Read article Abid

AbidPak-Qatar, EFU Takaful, Jubilee General Takaful, Dawood Family Takaful, and Salaam Takaful reviewed for Pakistani retail users.

Read article Abid

AbidMeezan, UBL, NIT, Alfalah, and MCB Arif Habib compared for Pakistanis choosing a retail mutual fund platform.

Read article Abid

AbidJS Global, AKD Securities, KTrade, Arif Habib Limited, and Finqalab reviewed through the lens of everyday retail investing in Pakistan.

Read article Abid

AbidRaast, 1LINK, PayPak, MNET Switch, and Visa / Mastercard explained through the payment rails Pakistanis use every day.

Read article Abid

AbidCompare Easypaisa, JazzCash, SadaPay, NayaPay, and Mashreq for retail payments, transfers, wallet use, fees, limits, and digital convenience in Pakistan.

Read article Abid

AbidCompare Mobilink, Telenor, U Microfinance Bank, Khushhali, and NRSP for retail microfinance banking, digital access, and financial inclusion in Pakistan.

Read article Abid

AbidCompare Meezan Bank, BankIslami, Dubai Islamic Bank Pakistan, Askari Bank Islamic, and Al Baraka for retail Islamic banking in Pakistan.

Read article Abid

AbidCompare HBL, UBL, Standard Chartered Pakistan, Allied Bank, and Bank Alfalah for retail banking, digital access, branch convenience, and everyday account use.

Read article Abid

AbidHBL Platinum, Bank Alfalah Ultra Cashback, Standard Chartered World, Askari World, and UBL Visa Infinite compared for new credit card users.

Read article Abid

AbidAvoid seven beginner mistakes that damage long-term returns in Pakistan, with practical risk controls and a safer execution checklist.

Read article Abid

AbidYour first 90 days as a Pakistani beginner investor, from emergency cash and account setup to allocation policy and review discipline.

Read articleBrowse Other Categories