Abid

Abid- 18 Apr, 2026

Top 5 Forex and CFD Brokers for Pakistanis

Pepperstone, IC Markets, Fusion Markets, Axi, and Exness compared for Pakistan-based traders weighing forex and CFD platforms.

Read articleCategory Archive

Understand global diversification, currency exposure, ETFs, and cross-border account considerations from Pakistan.

6 articles in this category.

AbidPepperstone, IC Markets, Fusion Markets, Axi, and Exness compared for Pakistan-based traders weighing forex and CFD platforms.

Read article Abid

AbidWise, Payoneer, Elevate Pay, nsave, and Fasset reviewed for Pakistan-based users who earn, hold, or move money across borders.

Read article Abid

AbidInteractive Brokers, CapTrader, Zacks Trade, TradeStation Global, and MEXEM assessed for Pakistan-based investors seeking global market access.

Read article Abid

AbidXPay, PayFast, HBLPay Checkout, Bank Alfalah IPG, and PayPro compared for online merchants accepting payments in Pakistan.

Read article Abid

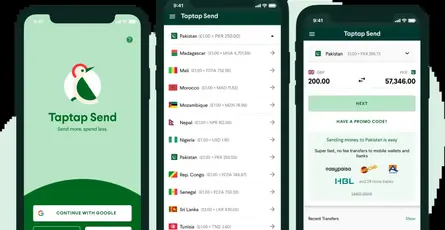

AbidTapTap Send, Remitly, WorldRemit, ACE Money Transfer, and MoneyGram compared for sending money to Pakistan.

Read article Abid

AbidBuild a disciplined global diversification plan from Pakistan using clear allocation rules, currency awareness, and regulatory caution.

Read articleBrowse Other Categories